Your credit score plays a major role in determining whether you qualify for a mortgage and what interest rate you’ll receive. But here’s the good news: there’s no single magic number that works for everyone. Different loan programs have different requirements, and understanding your options can help you find the right path to homeownership.

Understanding Townhouses and Single-Family Homes

Before comparing these housing options, it’s helpful to understand what makes each type unique.

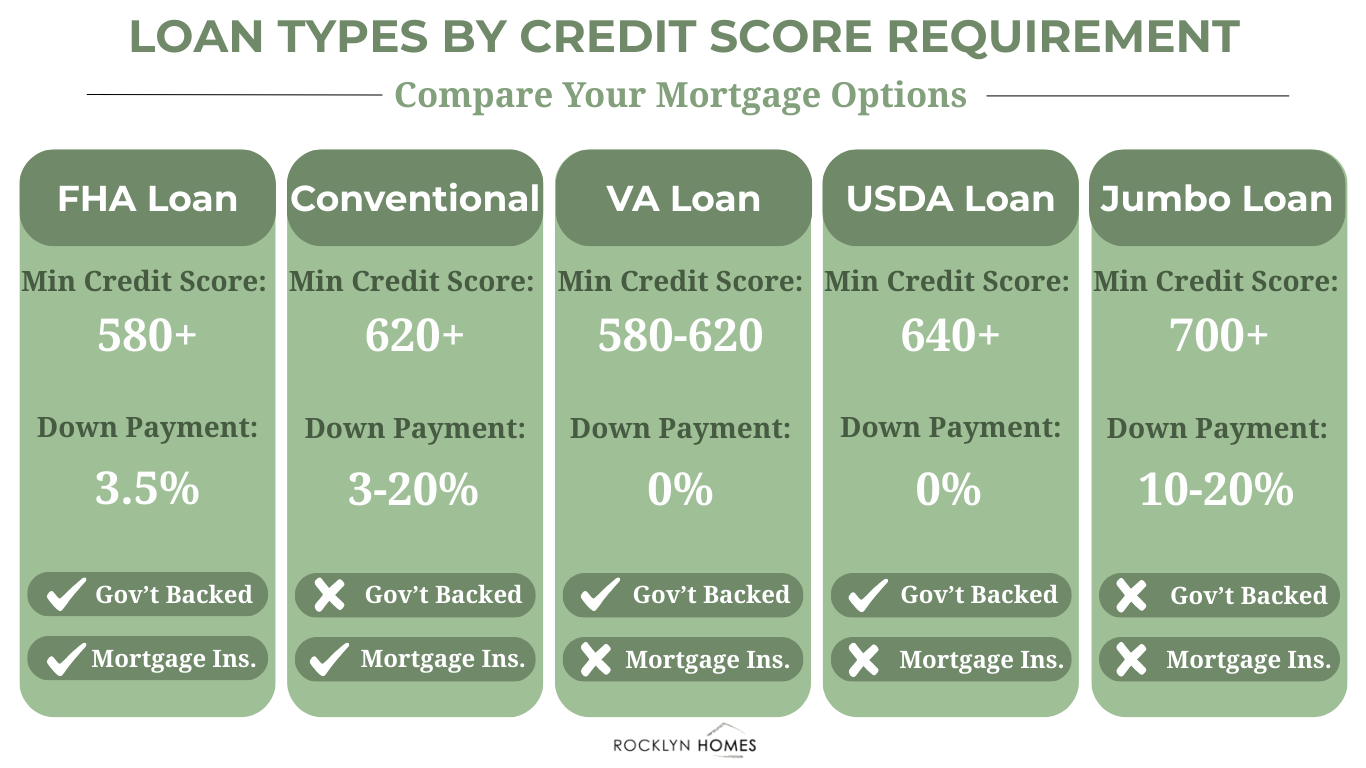

Credit Score Requirements by Loan Type

Each mortgage program has its own minimum credit score requirement. Your FICO score determines which programs you qualify for and how much you’ll pay in interest over the life of your loan.

FHA Loans

The Federal Housing Administration offers some of the most flexible credit requirements available. Borrowers with a credit score of 580 or higher qualify for just 3.5% down. Scores between 500 and 579 can still qualify, but you’ll need at least 10% down. FHA loans work well for first-time homebuyers and those rebuilding their credit history.

Conventional Loans

As of November 2025, Fannie Mae and Freddie Mac removed the hard 620 minimum credit score requirement for loans processed through their automated underwriting systems. However, most mortgage lenders still prefer borrowers with scores of 620 or above. Borrowers with scores below 620 may qualify if they have strong compensating factors like low debt-to-income ratios, significant savings, or stable employment.

VA Loans

The Department of Veterans Affairs doesn’t set a minimum credit score for VA loans. However, most VA lenders require scores between 580 and 620. These government-backed mortgages offer eligible veterans and service members excellent terms, including no down payment requirement and competitive interest rates.

USDA Loans

For buyers in rural areas, USDA loans offer zero down payment options. Most USDA lenders require a minimum credit score of 640 for automatic approval through the Guaranteed Underwriting System. Borrowers with lower scores may still qualify through manual underwriting with strong compensating factors.

Jumbo Loans

Jumbo loans finance homes that exceed conforming loan limits. Because these loans carry more risk for lenders, they require higher credit scores. Most jumbo lenders want to see scores of 700 or above, with the best rates going to borrowers with scores of 740 or higher

How Your Credit Score Affects Your Mortgage

Your credit score impacts more than just approval. It directly influences your interest rate, which affects your monthly payment and the total cost of your home over time.

Interest Rate Impact

A higher credit score typically means a lower interest rate. Even a small rate difference adds up significantly over a 30-year mortgage. Borrowers with excellent credit often qualify for rates a full percentage point lower than those with fair credit. On a 30-year mortgage, this difference could save tens of thousands over the life of the loan.

Private Mortgage Insurance

If your down payment is less than 20% on a conventional loan, you’ll pay private mortgage insurance. Your credit score affects how much PMI costs. Higher scores mean lower PMI premiums, reducing your monthly payment. FHA loans require mortgage insurance premiums regardless of your down payment amount.

Loan Terms and Options

Strong credit opens doors to better loan terms. Borrowers with higher scores often have access to more mortgage options, lower fees, and more flexible qualification requirements. A healthy credit history demonstrates to lenders that you’re likely to make on-time payments.

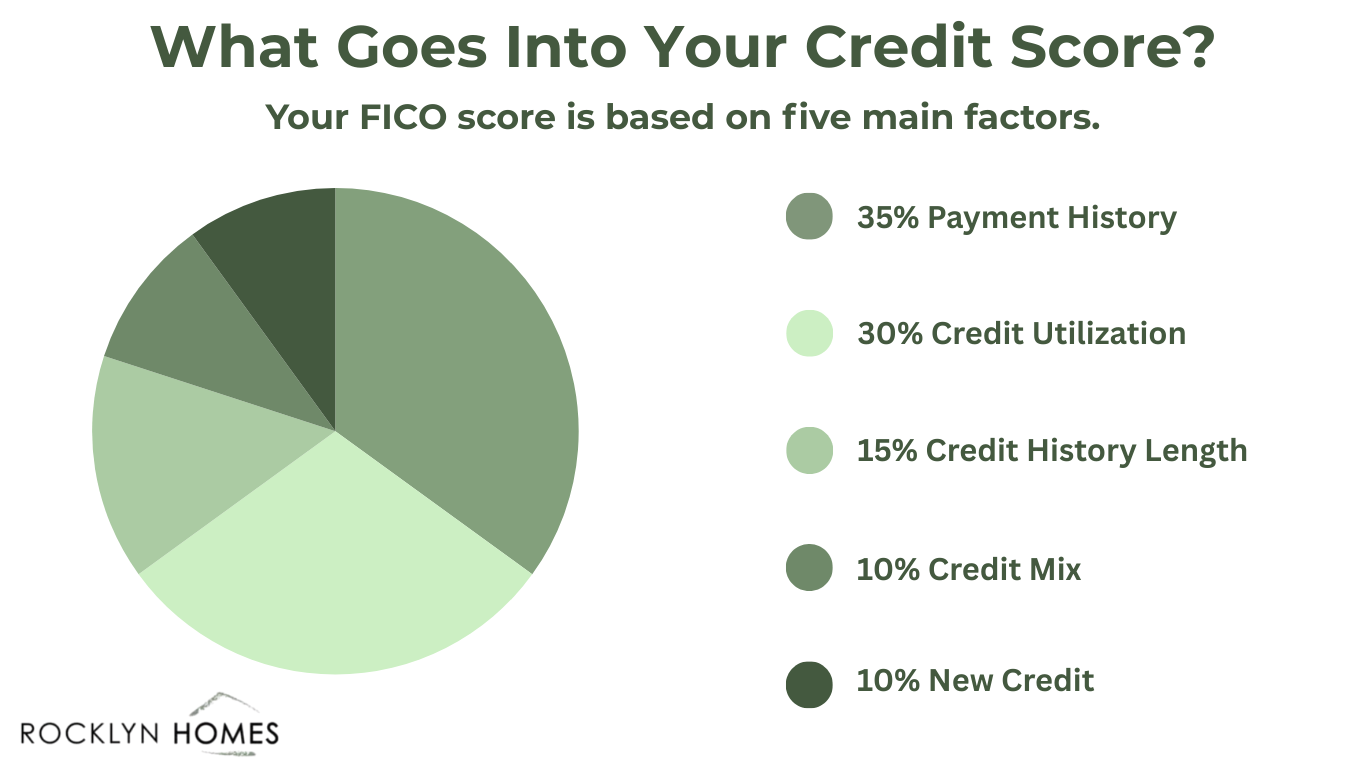

What Goes Into Your Credit Score

Understanding what shapes your credit score helps you improve it before applying for a mortgage. Your FICO score comes from five main factors.

- Payment History (35%): Your track record of paying bills on time matters most. Late payments, collections, and bankruptcies hurt your score the most.

- Credit Utilization (30%): This measures how much of your available credit you’re using. Keeping balances below 30% of your credit limit helps your score.

- Length of Credit History (15%): Longer credit histories generally help your score. This is why keeping older accounts open benefits you.

- Credit Mix (10%): Having different types of credit, like credit cards and installment loans, shows lenders you can manage various accounts.

- New Credit (10%): Opening several new accounts in a short time can temporarily lower your score. Space out new credit applications.

Steps to Improve Your Credit Score Before Buying

If your credit score needs work before you apply for a mortgage, focus on these strategies that deliver the fastest results.

Check Your Credit Report

Request your free credit report from all three bureaus: Experian, Equifax, and TransUnion. Review each report for errors, such as accounts that don’t belong to you or incorrect payment information. Disputing errors can boost your score quickly once corrections are made.

Pay Down Existing Debt

Reducing your credit card balances improves your credit utilization ratio. Focus on paying down cards with the highest utilization first. This single action can raise your score by 20 to 50 points within a billing cycle.

Make Every Payment On Time

Since payment history carries the most weight, prioritize paying all bills by their due dates. Setting up automatic payments helps you avoid missed deadlines. Even one late payment can significantly damage your score.

Avoid Opening New Credit

In the months leading up to your mortgage application, resist opening new credit accounts or making large purchases on credit. Each new application creates a hard inquiry on your report, and new accounts lower your average account age.

Rocklyn Homes: Your Partner in Homeownership

Finding the right home is just as important as finding the right financing. Rocklyn Homes builds quality new construction homes across Georgia, Florida, and Alabama designed for today’s families. Whether you’re a first-time homebuyer working with an FHA loan or an experienced buyer ready to build equity in a new home, Rocklyn Homes offers thoughtfully designed communities at accessible price points.Ready to start your homebuying journey? Visit Rocklyn Homes’ Buyer’s Guide to learn about the steps to homeownership, or connect with their preferred lender to discuss your financing options today.