The Short Answer: Assuming a mortgage means taking over a seller’s existing loan, including its interest rate and remaining balance. This option can save buyers real money when current rates are higher than the rate already locked in on the seller’s mortgage.

Mortgage assumption doesn’t come up in most homebuying conversations, but it’s worth knowing about. When interest rates rise, an assumable mortgage gives a buyer access to a lower rate locked in years earlier. That means a lower monthly payment without the cost of a brand-new mortgage. This guide covers what mortgage assumption is, which loan types qualify, how the process works, and when it actually makes financial sense. If you’re exploring financing options or comparing your choices before buying, this is a good place to start.

What Is an Assumable Mortgage?

An assumable mortgage allows a buyer to take over the seller’s existing mortgage loan instead of applying for a new one. The buyer steps into the original borrower’s position, inheriting the remaining mortgage balance, the original terms, and the existing interest rate. The seller’s mortgage effectively becomes the buyer’s mortgage.

This matters most when the seller locked in a lower interest rate years ago. If current rates on new loans are significantly higher, the buyer gains an immediate financial advantage by keeping the old rate through loan assumption rather than starting fresh with a brand-new mortgage.

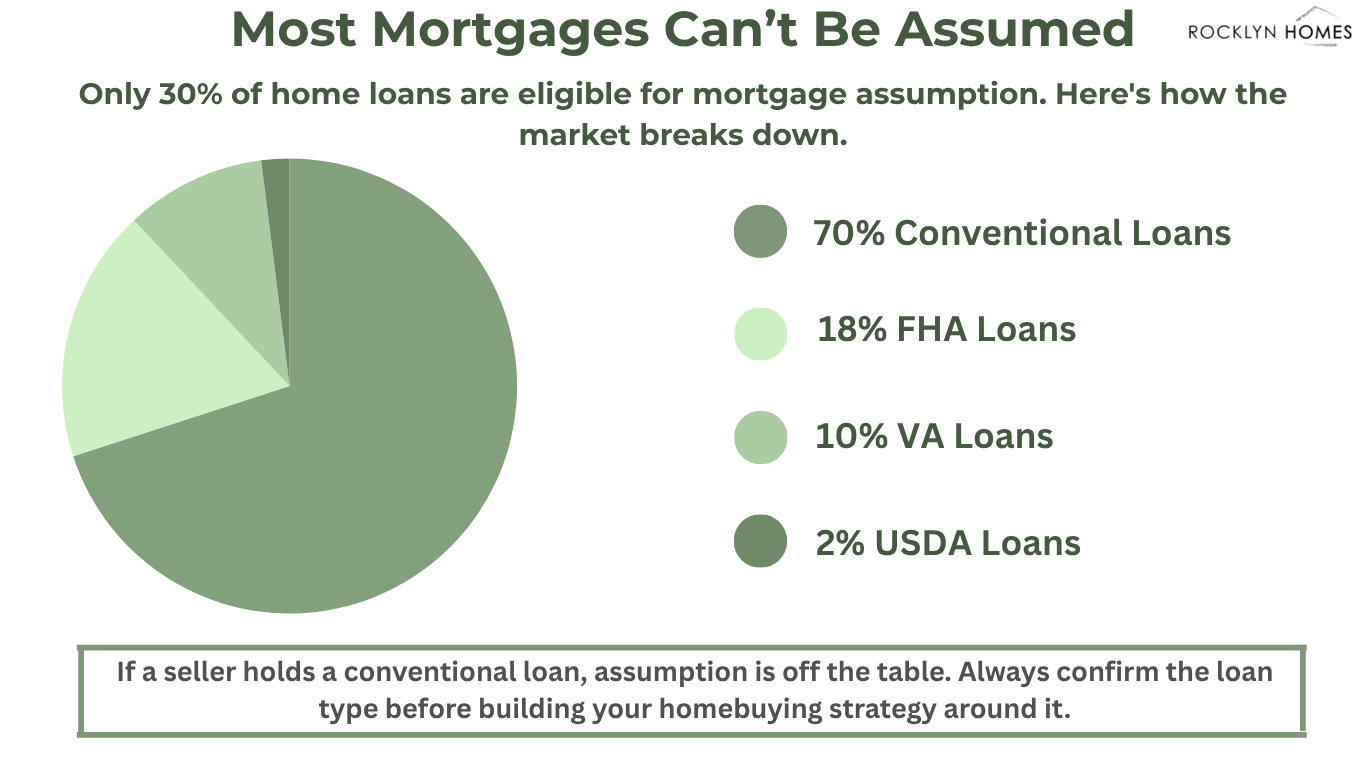

At a Glance: Assumable Loan Types

- FHA loans: Loans backed by the Federal Housing Administration are generally assumable with lender approval. Buyers must meet income requirements and credit standards set by the mortgage lender.

- VA loans: Loans through Veterans Affairs are assumable by both veterans and non-veterans. VA loan assumption comes with specific rules around VA entitlement that both parties should review carefully before proceeding.

- USDA loans: These government-backed loans are assumable under certain conditions and require lender approval.

- Conventional loans: Most conventional mortgages and conventional loans include a due-on-sale clause. This clause requires the full loan balance to be paid when the property is sold, making assumption impossible in most cases.

Government-backed mortgages are the main candidates for loan assumption. If a seller holds an FHA, VA, or USDA loan, assumption is worth exploring.

How to Assume a Mortgage: The Process

Mortgage assumption is not automatic. Buyers must apply through the mortgage lender and meet specific requirements before taking over an existing mortgage.

- Step 1 – Confirm the loan is assumable: Ask the seller or their agent whether the existing loan is government-backed. Review the loan documents for assumption language before moving forward.

- Step 2 – Contact the mortgage lender: Lender approval is required for any assumption. Reaching out early helps buyers understand what documentation is needed and how long the process typically takes.

- Step 3 – Submit an application: Buyers apply similarly to how they would for a new loan. Lenders review income, credit history, and debt-to-income ratio to confirm the buyer can handle the mortgage payments.

- Step 4 – Pay the assumption fee: Lenders charge an assumption fee to process the loan transfer. This fee is typically lower than the closing costs tied to a brand-new mortgage, which can reduce upfront expenses.

- Step 5 – Close the transaction: Once the lender approves the assumption, the assumed mortgage transfers to the buyer. If the lender issues a full release of liability, the original borrower is no longer responsible for the loan going forward.

Covering the Purchase Price Gap

A buyer assumes the seller’s remaining mortgage balance, not the full purchase price. If the home’s purchase price is higher than the existing mortgage balance, the buyer must cover the difference through savings, a second mortgage, or other financing. This gap can be significant in markets where home values have climbed well above the amount originally borrowed.

Pro Tip: Ask a mortgage lender to run the numbers comparing a new loan at current rates against an assumed loan. The monthly payment difference often tells the full story quickly.

When Assuming a Mortgage Makes Financial Sense

Loan assumption is not the right path for every buyer. But in the right situations, it delivers real financial advantages.

Rising Interest Rate Environment

If a seller secured a lower interest rate years ago and current rates are significantly higher, keeping that rate through assumption reduces monthly payments over the life of the loan. A seller with an FHA loan at 3.5% versus current rates near 7% could represent savings of several hundred dollars per month for the buyer.

Divorce Proceedings

When one spouse keeps the home after a divorce, assuming the existing mortgage avoids refinancing into a new loan at a higher rate. The spouse remaining in the home takes over the loan without triggering a new origination or incurring new loan costs.

Family Member Transfers

When property passes between family members, the new owner can assume the existing mortgage to keep the original terms and interest rate intact. This avoids the cost and rate exposure of starting over with a new loan.

Lower Upfront Costs

Assumption fees are generally lower than the closing costs on a new mortgage. Buyers looking to reduce what they spend upfront may find this advantage meaningful on its own, independent of the rate benefit.

Risks and Requirements to Know Before You Assume

Mortgage assumption offers real benefits, but buyers should go in with clear expectations.

VA Entitlement Rules

VA loans are assumable by veterans and non-veterans. When a non-veteran assumes a VA loan, the seller’s VA entitlement remains tied to that loan until it is fully paid off. This limits the seller’s ability to use their VA benefit on a future home purchase. In some cases, a veteran who assumes the loan can restore the seller’s entitlement. Reviewing the details with a Veterans Affairs lender before committing is a smart step. A surviving spouse may also qualify to assume a deceased veteran’s VA loan under specific conditions that vary by lender.

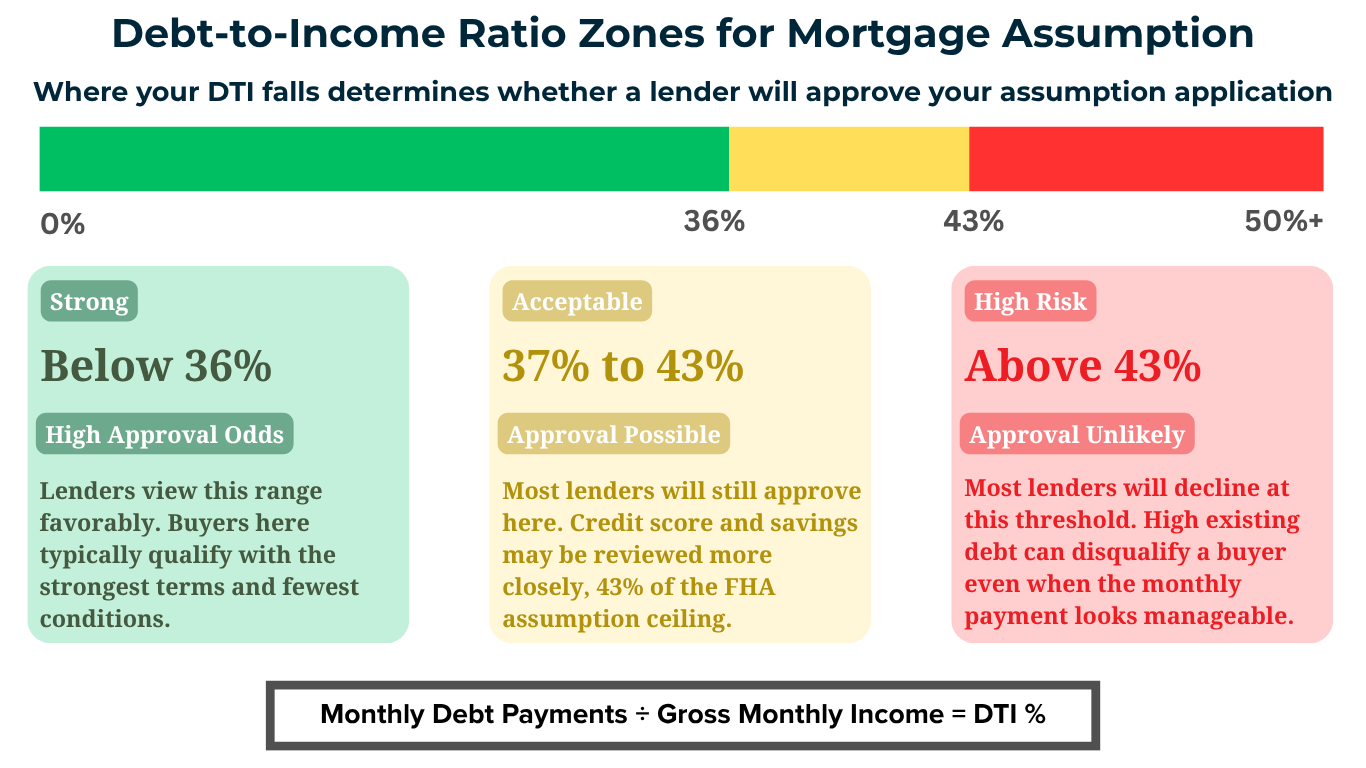

Income Requirements and Debt-to-Income Ratio

Lenders review the buyer’s debt-to-income ratio before approving an assumption. If the buyer carries significant existing debts, approval may be difficult even when the assumed mortgage’s monthly payment looks manageable on its own. Meeting the lender’s income requirements is not optional.

The Due-on-Sale Clause

Most conventional loans contain a due-on-sale clause that prevents assumption entirely. Always verify whether a loan is assumable before building a buying strategy around it. Assuming it qualifies without confirmation can create costly problems late in a transaction.

Legal Advice Matters

Mortgage assumption transfers a financial obligation from one party to another. Consulting a real estate attorney before finalizing any assumption agreement is a practical step, especially in cases involving divorce proceedings, estate transfers, or layered financing arrangements. Legal advice protects both parties and clarifies what each side is agreeing to before closing.

Rocklyn Homes: Your Partner in Smart Homebuying

Understanding your financing options is part of making a confident homebuying decision. Mortgage assumption is one tool worth knowing, especially when today’s interest rates are higher than they were in previous years. But for many buyers, particularly those purchasing new construction, new loan programs and preferred lender relationships offer strong paths to ownership as well.

Rocklyn Homes builds thoughtfully designed townhomes and single family homes throughout the Atlanta area. With a full-service design studio, buyers can personalize their home before it’s built. The Rocklyn team connects buyers with preferred lenders and walks them through available financing options, making the path to ownership clearer from day one.

If you’re ready to explore homeownership in a Rocklyn Homes community, browse current listings and connect with the Rocklyn team to find the home that fits your life. Contact Rocklyn Homes today to get started.