Buying a new construction home is exciting, but it also raises questions about how to protect your investment. Unlike purchasing an older home, a new build involves several stages where different types of coverage come into play.

Understanding your insurance options helps you avoid gaps in protection and prevents surprises at closing. This guide walks through the coverage types you may need, when each policy kicks in, and how working with a trusted home builder like Rocklyn Homes simplifies the path to owning your new home.

Understanding New Construction Insurance and Why It Matters

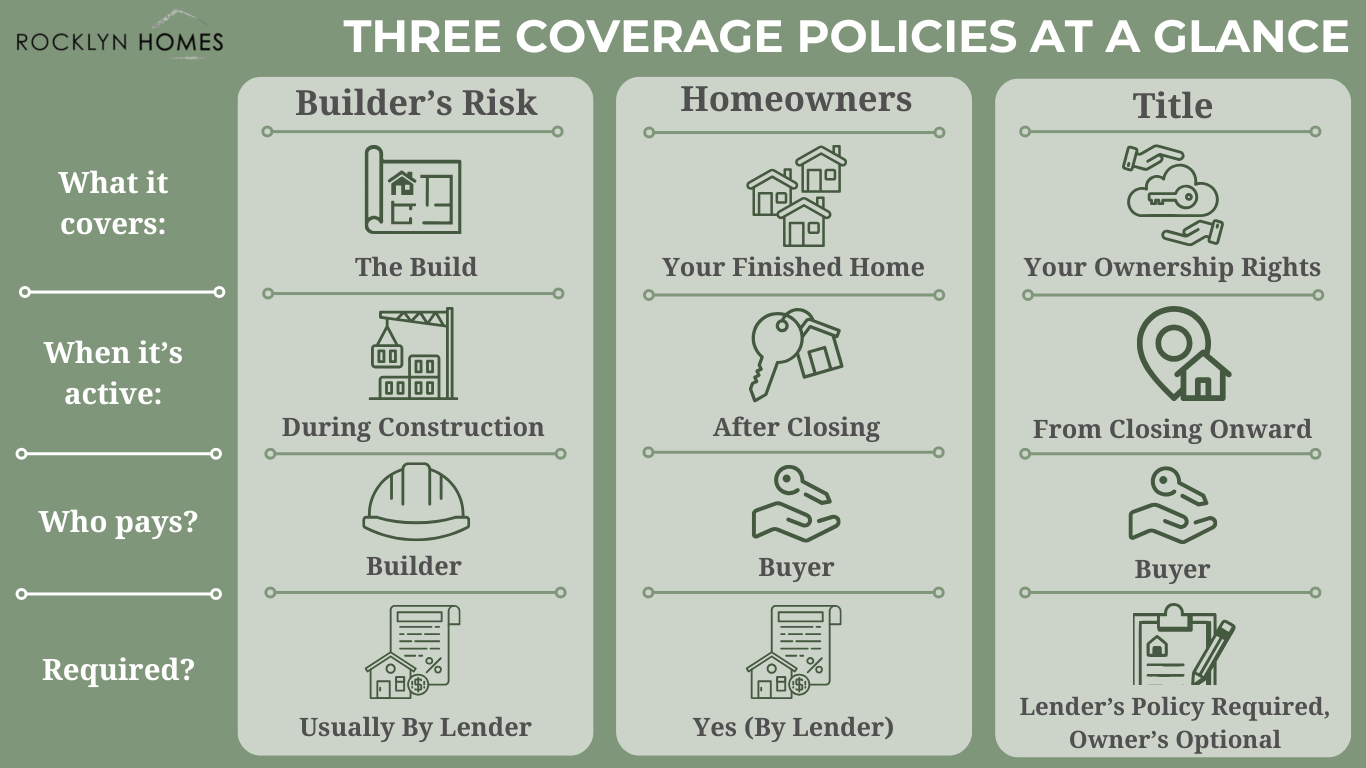

New construction insurance refers to the coverage options that protect a home before and after it is built. The term covers several policies, each designed for a specific stage of the construction process. Some policies protect the builder, while others protect the buyer or the lender.

Why Coverage Is Different for a New Build

A new construction home sits on an active construction site for months before it becomes your residence. During that time, construction materials, tools, and partially completed structures face risks like fire, theft, storm damage, or vandalism. A standard homeowners insurance policy does not cover these construction-phase risks. That is where builder’s risk insurance comes in.

Once the home is finished and you close on the property, homeowners insurance takes over as your main source of financial protection against property damage and liability claims.

Who Carries the Insurance at Each Stage

Responsibility for insurance shifts as the construction project progresses. Here is how it generally breaks down:

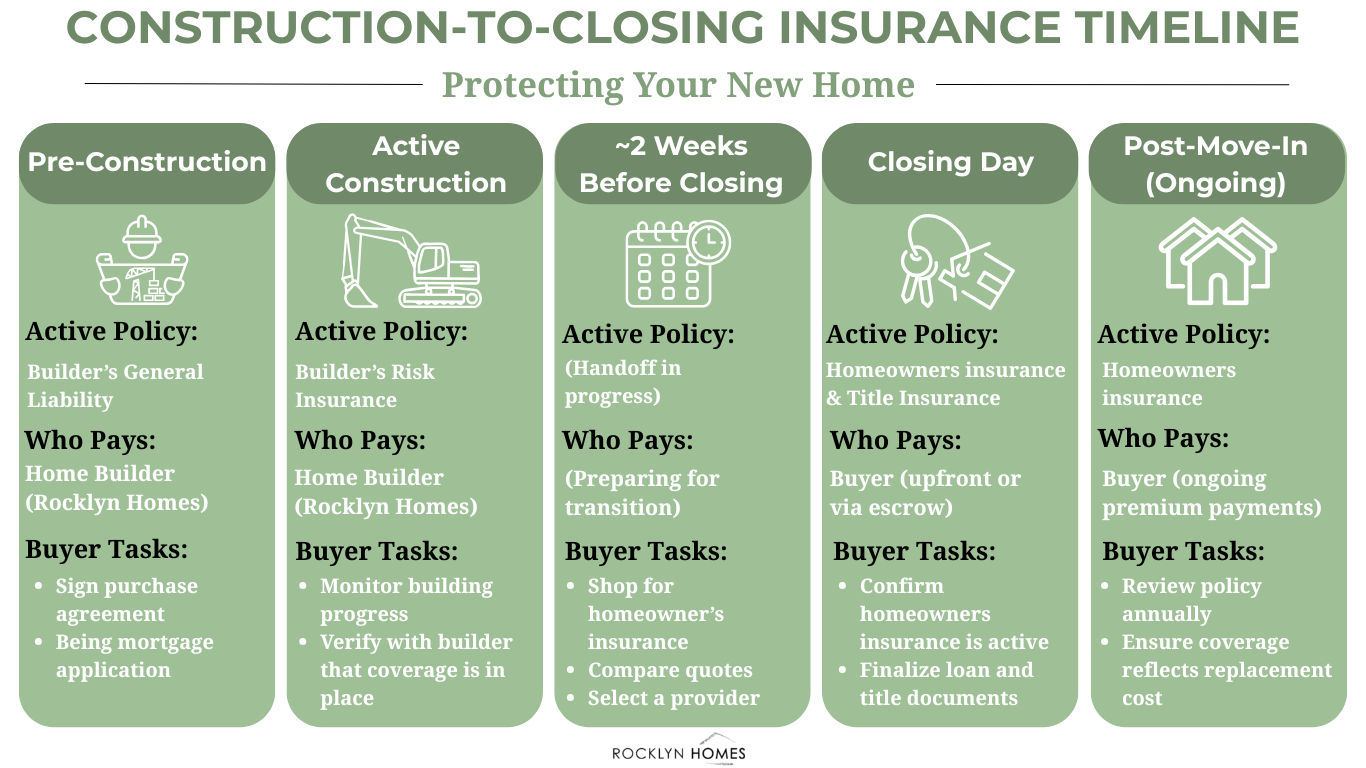

- During construction: The general contractor or home builder usually carries builder’s risk insurance and general liability insurance to protect the property, construction materials, and workers on site.

- At closing: The buyer secures homeowners insurance and title insurance, often coordinated with their lender.

After closing: The new property owner maintains homeowners insurance and any additional coverage based on their personal needs.

Types of Coverage for a New Construction Home

Several types of insurance may apply to a new construction project. Knowing what each policy covers helps you make informed decisions as a buyer.

Builder’s Risk Insurance

Builder’s risk insurance protects the home while it is under construction. This coverage option handles property damage from events like fire, wind, theft, and vandalism. It also protects construction materials stored on the construction site. Most home builders carry this coverage themselves, so buyers rarely need to buy it separately. Always confirm with your builder what their builder’s risk policy includes before signing a contract.

Homeowners Insurance

Homeowners insurance is the main coverage for your finished new home. Most lenders require this policy before closing on a new build. A standard homeowners insurance policy typically includes:

- Dwelling coverage: Pays to repair or rebuild your home after a covered loss.

- Personal property coverage: Protects your belongings inside the home.

- Liability coverage: Helps with legal costs if someone is injured on your property.

- Additional living expenses: Covers hotel or rental costs if you cannot live in your home after a covered event.

Shop around with multiple insurance providers to compare coverage limits and rates. A trusted insurance agent can help you pick the right coverage for your new home construction project.

Title Insurance

Title insurance protects your ownership rights. A title search before closing looks for title issues like a mechanics lien, boundary dispute, or unpaid taxes tied to the land. There are two types of title insurance policies:

- Owner’s policy: Protects the property owner for as long as they own the single-family home.

- Lender’s policy: Required by your mortgage lender and protects the loan amount against title issues.

Even on a brand-new home that has never been lived in, a title search can uncover issues related to the land itself. A construction endorsement can be added to your title insurance policy for extra protection during the new home construction phase.

Timing and Factors for Your Insurance Coverage

Knowing when to activate coverage and what affects your policy helps you plan ahead. A few details shape both your timing and your needed coverage limits.

When to Get Insurance During the Construction Process

Your builder typically carries builder’s risk and general liability insurance during the construction project. Once the home is close to completion, you will need to line up homeowners insurance. Most lenders require the policy to be active before they fund the loan.

Plan to secure a homeowners insurance policy about two weeks before closing. This gives you time to compare insurance providers and review coverage limits. Your insurance agent can coordinate the start date with your closing day so there is no gap in protection.

Location and Property Type

Where you build affects your coverage options. Homes in storm-prone regions may need extra wind or flood coverage. Townhomes often carry different policy structures than a single-family home, since some exterior maintenance falls under a homeowners association. Ask your insurance company how the property type affects your premium and coverage.

Replacement Cost and Personal Belongings

Your coverage limits should reflect the cost to rebuild your newer home, not the purchase price alone. A new build with updated materials and modern systems may cost more to replace than an older home of similar size. Talk to your insurance agent about replacement cost coverage rather than actual cash value.

Think about the value of your personal belongings, too. Families with high-value items like jewelry or electronics may want scheduled coverage. Higher liability coverage limits offer stronger protection if you host guests often or have features like a pool.

Financing Your New Home Through BankSouth Mortgage

At Rocklyn Homes, we believe buying a new construction home should feel clear and straightforward. Our team walks you through each step of the construction process, from design selections to closing day. While we do not sell insurance directly, we work closely with our preferred lender, BankSouth Mortgage, who helps coordinate homeowners insurance and title insurance for your new build.

The Smith-Rhoades Team at BankSouth Mortgage handles loan applications and helps buyers meet their lender’s insurance requirement before closing. Their team walks you through financing options, coordinates timing with your insurance agent, and answers questions about coverage tied to your mortgage.

Ready to start the journey toward owning a new home? Visit Rocklyn Homes to explore our current communities in Georgia and Florida. Contact our team or connect with BankSouth Mortgage to get guidance on financing and insurance requirements as you plan your new construction project.

Is homeowners insurance required for a new construction home?

Yes, most mortgage lenders require homeowners insurance before closing on a new construction home. The policy must be active on the closing date to protect the lender’s investment. Even cash buyers should carry homeowners insurance for their own financial protection against property damage and liability.

Does the builder’s insurance cover my new home during construction?

In most cases, yes. The general contractor or home builder carries builder’s risk insurance and general liability insurance during the construction process. These policies cover property damage, theft of construction materials, and on-site accidents. Always confirm coverage details with your builder before signing a contract.

When should I buy homeowners insurance for a new build?

Purchase homeowners insurance at least two weeks before your closing date. This gives you time to compare insurance providers, review coverage limits, and meet your lender’s insurance requirement. Your insurance agent can coordinate the policy start date with your closing.

Do I need title insurance on a new construction home?

Yes, title insurance is strongly recommended even on a brand-new single-family home. A title search can uncover issues like a mechanics lien, boundary dispute, or unpaid taxes on the land. Both an owner’s policy and a lender’s policy offer protection against title issues that could affect your ownership rights.

How does new construction insurance differ from coverage on an older home?

New construction insurance often includes a construction endorsement and may cost less because the home has updated systems and materials. Older home policies often have higher premiums due to outdated wiring, plumbing, or roofing. Insurance providers calculate rates based on risk, and a newer home generally presents lower risk than an older home.