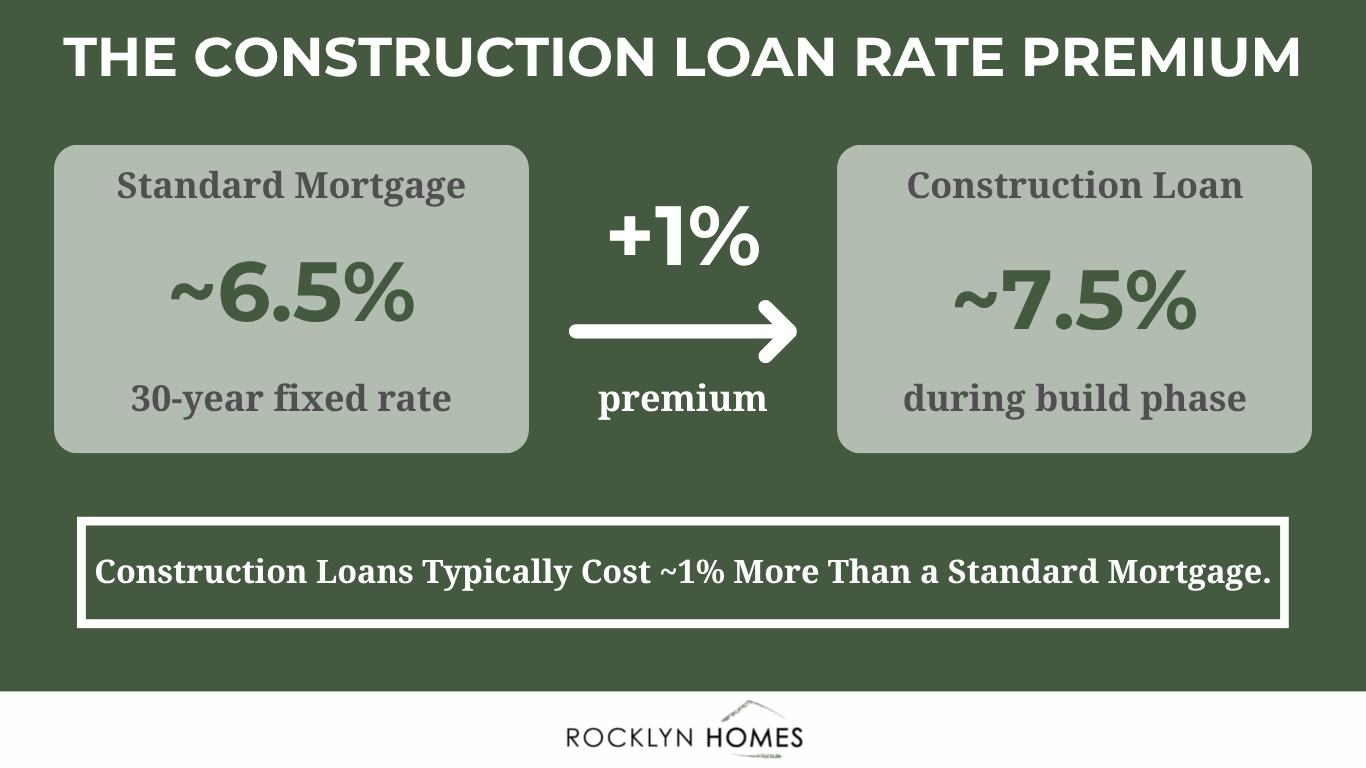

New construction loan rates in 2026 typically range from 6.5% to 9% for traditional bank lenders, sitting about 1% higher than standard mortgage rates because of the added risk lenders take during the building phase. Your final rate depends on your credit score, down payment, debt-to-income ratio, and the type of loan you choose.

Buying a brand-new home is one of the most exciting steps you can take, but the financing side can feel confusing for first-time buyers. The term “new construction loan rates” gets used a lot, yet the way these loans work differs from a traditional mortgage in some big ways. Understanding how interest rates apply, when payments begin, and what lenders look for can save you thousands over the life of your loan.

What Are New Construction Loan Rates?

A construction loan is a short-term loan that covers the cost of building a new home. Construction loan rates are the interest rates lenders charge for that financing. As of 2026, most construction loans carry rates between 6.5% and 9% through traditional banks and credit unions, though private lenders may charge up to 15%.

How Do They Differ From a Traditional Mortgage?

Traditional mortgages fund the purchase of an existing home with one closing and one rate locked in for the loan term. A construction loan works differently in several ways.

- Shorter loan term: Most construction loans last 12 to 18 months, just long enough to finish the build.

- Variable rates: Many construction loans use an adjustable-rate mortgage structure tied to the prime rate.

- Interest-only payments: During the construction phase, you only pay interest on the amount drawn so far.

- Two closings sometimes: Some loans require a second closing to convert to permanent financing.

How Do Construction Loan Rates Work During Building?

Construction loans use a draw schedule, where funds release in stages as the building progresses. Your interest only applies to the amount drawn at each stage, not the full loan amount.

Understanding the Draw Schedule

A typical draw schedule releases money in four to six phases. Each phase requires inspection before the next disbursement.

- Foundation pour: The first major draw covers excavation and foundation work.

- Framing complete: The second draw funds the structural shell.

- Mechanical rough-ins: Plumbing, electrical, and HVAC installations get funded here.

- Drywall and finishes: Interior work nears completion at this stage.

- Final inspection: The last disbursement closes out the build.

Monthly Interest-Only Payments

During the construction period, your monthly payment covers only interest on funds already drawn. If you have a $300,000 loan but only $60,000 has been drawn, your interest payment is calculated on that smaller amount. This keeps your actual payment obligation lower while the home is being built. Once construction wraps up, your loan either pays off or converts to a permanent mortgage with a fixed monthly payment.

What Factors Affect Your Construction Loan Rate?

Several things shape the rate you receive at loan closing. Lenders weigh each one to assess risk before approving your loan amount.

Your Credit Score and Financial Profile

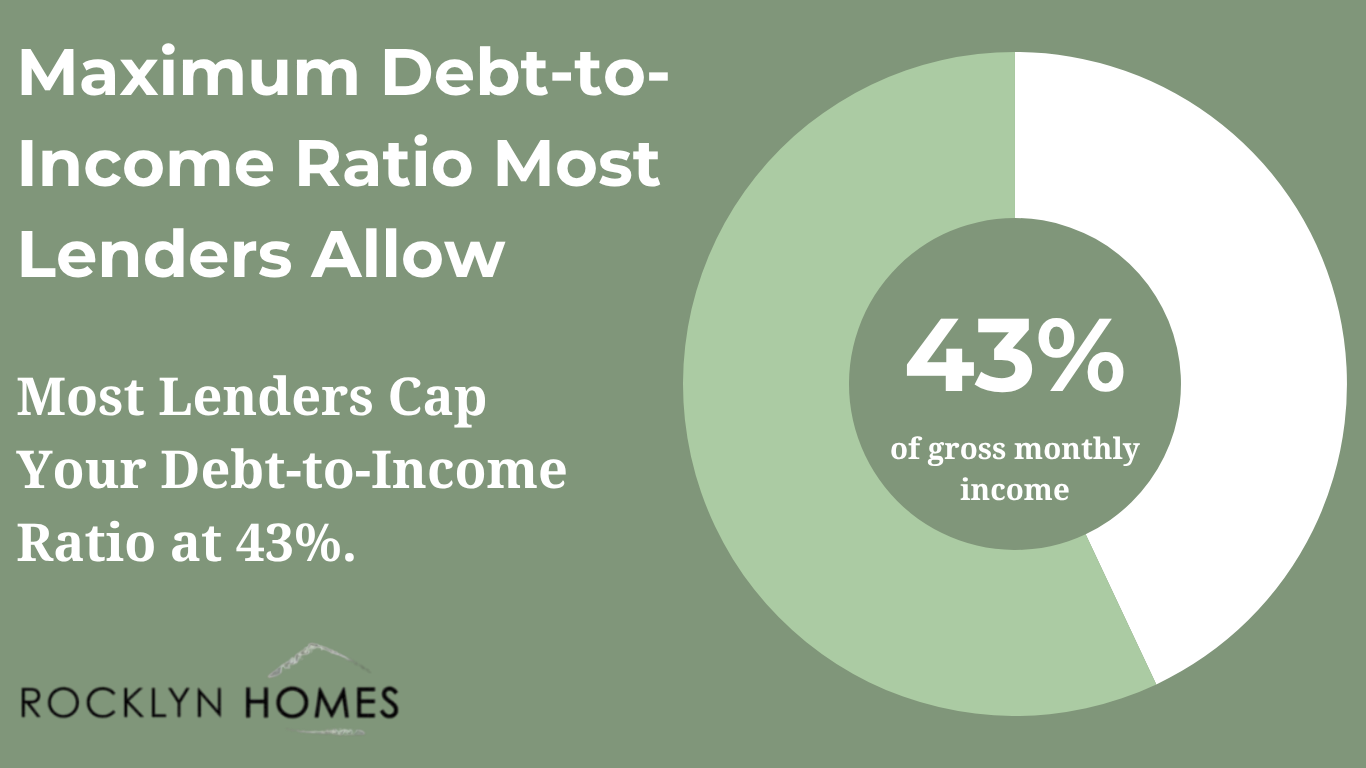

Lenders prefer borrowers with strong credit history because construction loans carry more risk than standard mortgages. Most banks want a credit score of 680 or higher, with the best rates going to scores above 740. Your debt-to-income ratio matters just as much. Lenders generally cap this at 43% to 45%. Carrying balances on credit cards or large personal loans can push your ratio higher and limit your loan amount.

Down Payment and Loan Amount

Construction loans typically require 20% to 25% down. A larger down payment lowers your loan-to-value ratio and qualifies you for competitive rates. Smaller loan amounts under conforming limits often get better pricing than jumbo construction loans.

Loan Type and Term

A construction-to-permanent loan often carries a slightly higher rate than a two-close construction loan because the lender locks the rate for both phases. Shorter loan terms also tend to receive lower interest rates than 30-year fixed options.

What Are the Main Types of New Construction Loans?

Not every new home purchase requires the same loan. Here are the most common options first-time buyers see when shopping for a primary residence.

Construction-to-Permanent Loan

This loan funds construction and automatically converts to a permanent loan once the home is finished. You only go through one credit approval and one loan closing. Many buyers prefer this option because it locks in your interest rate early and avoids a second closing fee.

Construction-Only Loan

A construction-only loan funds the build, then must be paid off when construction ends. Buyers then apply for a separate permanent mortgage. This option gives you flexibility to shop for the best permanent financing later, but you face two sets of closing costs and the risk of rate changes.

Buying a Production-Built New Home

If you buy a brand-new home from a builder like Rocklyn Homes, you usually do not need a construction loan at all. The builder finances construction itself. You apply for a traditional mortgage loan, just like buying an existing home. This is often the simplest path to homeownership in a new home community.

Rocklyn Homes: Your Partner in New Construction Homebuying

Rocklyn Homes builds new construction townhomes and single-family homes across Georgia and Florida, offering first-time buyers a straightforward path to homeownership. Because Rocklyn handles the construction process from start to finish, you do not need to navigate a difficult construction loan. Instead, you work with our preferred mortgage lender, BankSouth Mortgage, to secure a standard mortgage loan on your finished home.

When you finance through BankSouth Mortgage, Rocklyn Homes also offers incentives that include closing cost contributions up to $15,000, depending on community and program eligibility. BankSouth offers a range of loan products including 30-year fixed-rate, adjustable-rate mortgage options, FHA, VA, and USDA loans for buyers who qualify.

Ready to explore new construction homes that fit your budget and lifestyle? Visit Rocklyn Homes to browse current communities, use our mortgage calculator, or connect with a community sales manager to start your pre-approval today.

What is a good interest rate for a new construction loan in 2026?

A good rate for a new construction loan in 2026 falls between 6.5% and 8% from traditional banks for borrowers with strong credit. Rates above 9% are common for private lenders or borrowers with lower credit scores. Your actual rate depends on your credit score, down payment, and loan type.

Are construction loan rates higher than traditional mortgage rates?

Yes, construction loans typically run about 1% higher than traditional mortgage rates. This reflects the added risk lenders take when financing a home that does not yet exist. Once your loan converts to permanent financing, the rate often adjusts to match standard mortgage pricing.

Do I need a construction loan to buy a new construction home from a builder?

No, you usually do not need a construction loan when buying from a production builder like Rocklyn Homes. The builder finances construction, and you simply apply for a standard mortgage loan on the finished home. This makes buying a new home much easier for first-time buyers.

What credit score do I need for a new construction loan?

Most lenders require a minimum credit score of 680 for a new construction loan, though 700 or higher is preferred. Buyers with scores above 740 often qualify for the most competitive rates. Strong credit also helps you secure better loan terms and lower insurance premiums.

How much down payment do I need for a new construction loan?

Construction loans typically require 20% to 25% down, which is more than a standard mortgage. However, if you buy a finished new home from a builder, you may qualify for traditional loan programs that allow as little as 3% to 5% down for first-time buyers.